- The Sovereign Signal

- Posts

- $190B Sold, VIX at 30, USD Reserves at Century Lows, USD/JPY Flirting With 160: Why This Is One Integrated Liquidity Event, Not Random Macro Noise

$190B Sold, VIX at 30, USD Reserves at Century Lows, USD/JPY Flirting With 160: Why This Is One Integrated Liquidity Event, Not Random Macro Noise

This is not a collection of macro anecdotes. It is one story. And the story is that the largest, most hyperconnected debt-and-leverage super-cycle in history is running into a liquidity problem that began with the Iran war and is now spreading through the system.

Luke Lovett

March 30, 2026

This is not a collection of macro anecdotes.

It is one story.

And the story is that the largest, most hyperconnected debt-and-leverage super-cycle in history is running into a liquidity problem that began with the Iran war and is now spreading through the system.

At first, the market treated the war the way stressed systems usually do.

Oil moved higher.

Volatility rose.

And gold and silver got sold for liquidity.

That was the tell.

Metals were not yet being bought as protection.

They were being used as funding sources inside a tightening system.

That is what happens when liquidity starts disappearing.

And in a system this levered, liquidity is not a side issue.

It is the whole game.

Because this system is built on:

refinancing

rollover

cheap funding

smooth collateral flows

and the assumption that the plumbing underneath global markets remains stable enough to absorb shocks

That is the illusion.

And when that illusion starts breaking, leverage gets crushed.

That is why Japan matters so much.

Japan is not just another country with a weak currency.

Japan is one of the key hidden funding anchors of the modern financial system. The carry trade rests on the assumption that Japan can keep supplying cheap, stable funding to the world.

Borrow cheap.

Fund risk.

Trust the base layer.

But now that base layer is wobbling.

USD/JPY broke 160.

Japanese officials are jawboning hard.

Japanese yields are rising.

And when Japan starts threatening “bold action,” what they are really telling you is simple:

the liquidity machine is not running smoothly anymore.

That matters because once the cheap-funding machine starts choking, everything financed on top of it becomes more fragile.

And that is exactly what we are seeing.

The bond market is under pressure.

Long-duration bonds just saw the second-largest outflow on record.

High yield has seen three straight weeks of outflows.

Treasury auctions are softening.

The U.S. 10-year is pressing higher.

That is not random.

That is the base layer of the system getting less stable.

And when the base layer gets less stable, the rest of the structure does not stay calm.

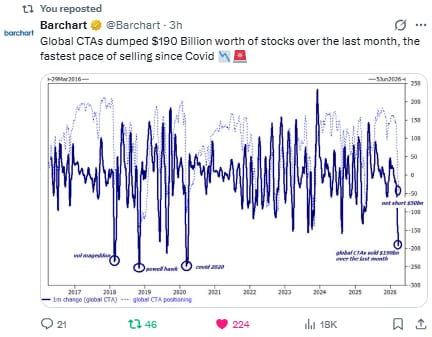

That is why the CTA selling matters.

That is why the CTA selling matters too.

$190 billion dumped from stocks in a month means one of the big mechanical buyers in the system is now a mechanical seller. The machines that usually help keep markets orderly are now reinforcing instability.

That is how corrections turn into air pockets.

And that brings us to Rory’s post, which is one of the most important framing devices in the whole discussion.

The “air pocket” moving through oil flows is not just a shipping concept.

It is a timeline of transmission.

East Asia first.

Then Europe.

Then North America.

That matters enormously.

Because the shock does not hit the whole world at once.

It rolls through the system in waves.

And in the most leveraged global economy ever built, that delay is not comforting.

It is dangerous.

Because it gives markets just enough time to remain complacent while the stress moves from one demand center to the next. By the time one region fully feels it, another is already deep into the consequences.

That is how a supply disruption becomes a macro event.

The air pocket lands first in the most import-sensitive nodes, then works its way through the rest of the system. And each step compounds the next:

supply gap

→ higher energy costs

→ tighter importer conditions

→ more inflation persistence

→ higher yield sensitivity

→ weaker growth

That is how a shipping disruption becomes a bond-market story in the biggest debt-and-leverage super-cycle ever.

And while all of this is happening, another structural pressure is sitting quietly underneath it:

Access the Signal Behind the Distortion

Debt-fueled distortions are warping stocks, credit, and global liquidity. We track the structural signals building beneath the surface — gold, silver, and the asymmetric setups mainstream coverage overlooks.

Already a paying subscriber? Sign In.

Reply