- The Sovereign Signal

- Posts

- Another ≈3% OF COMEX Silver GONE (could hit ZERO by March 6), One Step Closer To Global Margin Call Sparked By Japan, 87% of Global Bonds Now Generating Under 5% Returns

Another ≈3% OF COMEX Silver GONE (could hit ZERO by March 6), One Step Closer To Global Margin Call Sparked By Japan, 87% of Global Bonds Now Generating Under 5% Returns

Luke Lovett

February 19, 2026

ANOTHER ≈3% OF COMEX SILVER GONE🚨

~3M oz pulled from registered; “settleable” silver now ~88M oz.

WHAT IT ACTUALLY MEANS

Registered = deliverable now (the settlement layer)

Drain registered → fewer real ounces backing the paper stack

Price can stall while metal disappears because paper sets the print

Paper volume ≠ physical availability

Tight deliverable float → spreads widen → volatility jumps

SOVEREIGN DEBT BACKDROP

We’re in an escalating sovereign debt crisis inside the most hyper-interconnected, debt-saturated system ever.

Japan is the weak link → yen move = margin call fuel (yen carry unwind 2.0) → forced selling across everything.

That forces bigger policy response → currency debasement as the only pressure valve.

China real estate bleeding → more liquidity → global spillover → rate cuts spreading before downturn.

All of this is massively bullish for silver (and gold).

ONE STEP CLOSER TO JAPAN STARTING A GLOBAL MARGIN CALL

WHAT IT ACTUALLY MEANS

This is a plumbing tell: they’re checking dealer balance sheet capacity

“Quotes” = who can warehouse risk when the tape gets violent

USD/JPY is not a currency pair right now… it’s a liquidity valve

Yen squeezes = leveraged trades unwind = everything gets sold

Yen move → margin calls → forced liquidation = “safe havens” can drop too

WHAT BREAKS FIRST

First: funding markets price stress (basis, spreads, swap lines whispers)

Then: carry trades cough up assets (tech/credit/liquids first)

Then: policy tries to cap the yen move to slow contagion

Then: credibility test — can they “stabilize” without breaking something else?

Read between the lines: they’re protecting the settlement layer, not “FX optics.”

SOVEREIGN DEBT BACKDROP

What happens if the yen suddenly gets stronger

If the yen gets stronger, investors suddenly owe more in “real terms.”

That’s a currency shock.

Why that creates margin calls (the “forced selling” part)

Most of these investors are using leverage (borrowed money on top of borrowed money).

So when the yen jumps:

their trade starts losing money fast

the broker says: “Add more cash right now or we sell your stuff.”

That broker demand is a margin call.

If they don’t have cash sitting around, they sell whatever they can sell fastest:

stocks

gold

silver

anything liquid

That’s why we sometimes see everything drop at once.

Why Japan is the “weak link”

Because so much of the world’s leverage is tied to cheap yen borrowing.

So if the yen moves hard:

it doesn’t just hit Japan

it hits everyone’s borrowed-money trades worldwide.

That’s why “when the yen moves, liquidity moves.”

WHAT THE FED/TREASURY MUST DO IF IT ACCELERATES

They’ll lean on dealers first: “coordination,” jawboning, liquidity assurances

Then: intervention attempts to smooth, not “reverse,” the yen

If it fails: broader backstops (swap lines, repo capacity, collateral flexibility)

Because the real job is preventing a global forced-selling cascade ⚙️

It can only be prevented for so long.

In the meantime, more and more debt and leverage will continue to stack up to set up more vicious unwinds.

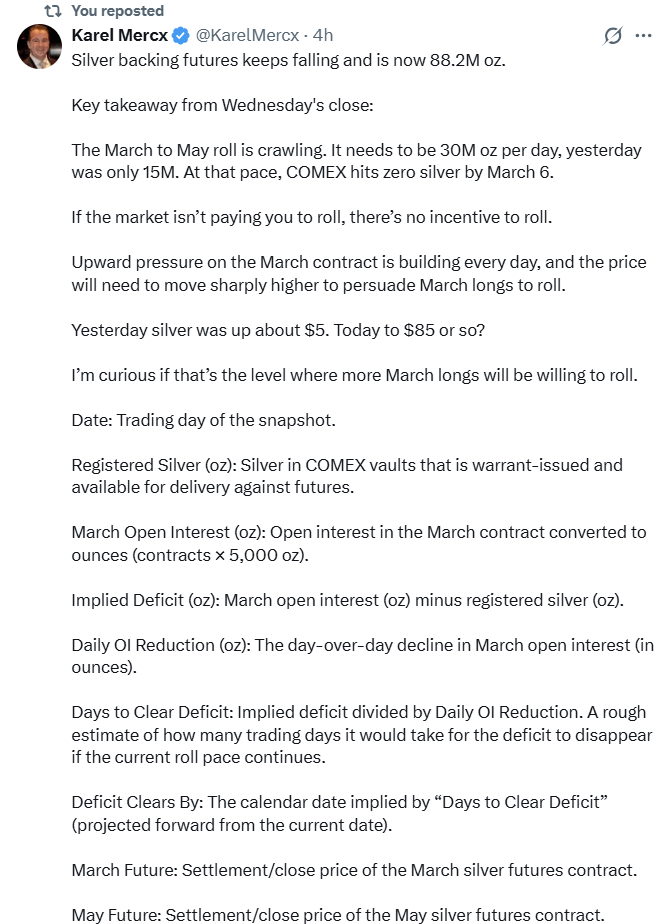

MARCH SILVER ROLL FAILS = SETTLEMENT STRESS BUILDS

WHAT THEY SAID

Silver backing futures keeps falling: ~88.2M oz

March→May roll “needs” ~30M oz/day

Latest pace: ~15M oz/day

At that pace: COMEX “hits zero” by March 6

WHAT IT ACTUALLY MEANS

Rolling = “I’ll take May paper instead of March metal.”

If the market won’t PAY you to roll, you don’t roll.

So March longs sit tight → nearby gets squeezed.

Slow roll + shrinking registered → March premium builds → price must jump.

Roll stalls → spreads flip → delivery stress shows up first.

…they’re trying to buy time with paper… while metal keeps leaving.

SOVEREIGN DEBT BACKDROP

We’re in an escalating sovereign debt crisis inside the most hyper-interconnected, debt-saturated global system ever.

There is a corresponding shortage of pristine collateral.

Silver is the most undervalued pristine collateral.

The market is just starting to figure this out.

WHAT BREAKS FIRST

First: March–May spread starts acting “wrong” (nearby tightness).

Then: liquidity air-pockets → violent intraday moves that look “random.”

Then: exchange incentives (margin hikes / rule tweaks) to force weak hands out.

Finally: more off-exchange sourcing (direct-to-refiner / direct-to-miner) as trust erodes.

LOW YIELDS + STICKY INFLATION = SOVEREIGN DEBT TRAP

WHAT IT ACTUALLY MEANS

This isn’t “a boring bond stat.”

It’s a pricing message.

Low yields = bond markets assuming: slower growth + future cuts + policy support.

But sticky inflation + giant debt loads = policy can’t normalize without something breaking.

So the system picks the pressure valve: financial repression (returns that look positive, but lose to reality).

Debt load + low yields → policymakers need rates lower → savers subsidize the system.

…“sub-zero yields” isn’t a market forecast — it’s a policy outcome when debt is too big to carry.

SOVEREIGN DEBT BACKDROP

The lower the returns in bonds, the more debt we need to get the same dollar of growth.

Which creates greater fragility in markets and sets up a more vicious unwind during the next downturn.

That forces bigger policy responses than ever → currency debasement becomes the only pressure valve.

Also, the lower the returns in bonds, the more likely investors re-allocate percentages of capital in bonds towards gold.

Returns in bonds will continue to decline.

MONEY SUPPLY OUTRUNS REAL OUTPUT—COSTS REPRICE LIKE CLOCKWORK

Car insurance is +56.1% since Nov 2019 while M1 sits at ~$19.1T (Dec 2025).

WHAT IT ACTUALLY MEANS

This is monetary gravity, not “greedy companies.”

Too many dollars chasing the same real stuff = price ladder.

M1 went vertical post-2020 and still sits around $19.1T.

Money growth > real output growth → purchasing power bleeds.

Read between the lines: the unit of account is wobbling, not just CPI baskets.

WHAT BREAKS FIRST

First: household balance sheets (insurance/energy/food) → confidence cracks.

Then: “safe” savings loses ground → people reach for risk or hard assets.

Then: governments lean harder on financial repression (yields down, deficits up).

Then: volatility spikes when the system tries to delever.

Why I Use HardAssets Alliance

HardAssets Alliance provides:

100% insurance of metals for market value

Institutional-grade daily audits and security

Best pricing — live bids from global wholesalers

Fully allocated metal — in your name, your bars

Delivery anytime or vault-secured across 5 global hubs

Luke Lovett

Cell: 704.497.7324

Undervalued Assets | Sovereign Signal

Email: [email protected]

Disclaimer:

This content is for educational purposes only—not financial, legal, tax, or investment advice. I’m not a licensed advisor, and nothing herein should be relied upon to make investment decisions. Markets change fast. While accuracy is the goal, no guarantees are made. Past performance ≠ future results. Some insights paraphrase third-party experts for commentary—without endorsement or affiliation. Always do your own research and consult a licensed professional before investing. I do not sell metals, process transactions, or hold funds. All orders go directly through licensed dealers.

Reply