- The Sovereign Signal

- Posts

- From “Risk‐Free” to Resource‐Short: What Bond Markets Are Telling Us About the End of This Regime

From “Risk‐Free” to Resource‐Short: What Bond Markets Are Telling Us About the End of This Regime

Why the next decade of returns will belong to those who rotate from paper promises to real constraints.

Luke Lovett

April 14, 2026

The way this cycle ends is not with one big headline, but with a slow, relentless repricing of what is real versus what is promised.

For five plus decades we optimized the world for efficiency and leverage.

We built a dollar‑centric stack of claims on top of a supply system that assumed cheap energy, open sea lanes, and politically neutral chokepoints.

Every basis point of lower volatility and every turn of extra leverage rested on that assumption.

That assumption is gone.

The Iran war, the Gulf disruptions, the rerouting of LNG and helium, the rolling accidents in aluminum and copper, the fertilizer and grain scares—these are not isolated “event risks.”

They are the failure modes of a just‑in‑time, single‑point‑of‑failure architecture colliding with great‑power politics.

The system can still function, but only by routing flows through longer, riskier, more capital‑intensive paths.

We haven’t lost capacity; we’ve lost optionality.

At the same time, the top of the stack has never been heavier.

The US is running 1–2T deficits before the full war bill, with interest costs compounding and no political constituency for genuine austerity.

Europe and Japan are no better; they just outsource more of the adjustment to their exchange rates and imported energy bills.

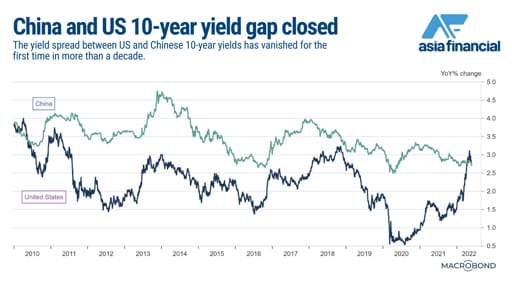

Bond markets are no longer indifferent: term premia are quietly rebuilding, and for the first time in decades we are seeing a credible alternative “haven” emerge in Chinese government paper.

This is the core tension of the debt super-cycle: the system needs negative real rates to roll the debt, but the system is now structurally short the very things—energy, metals, secure logistics—that push real prices up.

Every time we paper over a chokepoint with more capex, more inventory, more redundancy, we are choosing higher nominal paths and larger future issuance.

Financial repression is not a policy choice at the margin; it is becoming the only coherent endgame.

We see that tension most clearly in the currency complex.

The first instinct of global capital is still reflexive: oil spikes, war headlines hit, and the dollar catches a bid. Bunds and JGBs wear the pain, USTs get a tactical bid from domestic flows, and gold and silver are sold to meet margin and “reduce risk.”

It is the same Pavlovian trade that worked for a generation.

But under this regime it can’t be the last trade.

If oil and other inputs stay structurally dear; if we keep substituting “secure” US and allied supply for cheap Gulf and Eurasian supply; if deficits stay wide and term yields keep grinding higher—then the cost of that strong‑dollar reflex starts to exceed its benefit.

A reserve currency that has to live permanently at the high end of the real‑rate and energy‑cost distribution will end up dragging its own industrial base and fiscal math into the ditch.

At some point, the marginal holder will decide that 4–5% in a structurally debasing unit, backed by an overstretched sovereign and an eroding external position, is not a free lunch.

When that inflection comes, it will not announce itself with a crash in the DXY so much as a failure to make new highs in response to new shocks.

Access the Signal Behind the Distortion

Debt-fueled distortions are warping stocks, credit, and global liquidity. We track the structural signals building beneath the surface — gold, silver, and the asymmetric setups mainstream coverage overlooks.

Already a paying subscriber? Sign In.

Reply