- The Sovereign Signal

- Posts

- Japan’s Funding Anchor Is Buckling, Ares Gates $10.7B Fund, Hormuz Is Now A Paid Corridor, Mar26 Silver Delivers 44.17M Oz, China Pulls 790+ Tonnes, And The Market Still Hasn’t Priced How Fragile The Physical/Paper Split Has Become

Japan’s Funding Anchor Is Buckling, Ares Gates $10.7B Fund, Hormuz Is Now A Paid Corridor, Mar26 Silver Delivers 44.17M Oz, China Pulls 790+ Tonnes, And The Market Still Hasn’t Priced How Fragile The Physical/Paper Split Has Become

This market continues to look less and less like deep liquidity and more and more like connected reservoirs trying to keep pressure balanced.

Luke Lovett

March 24, 2026

This market continues to look less and less like deep liquidity and more and more like connected reservoirs trying to keep pressure balanced.

That is the real story.

Not one bad chart.

Not one scary headline.

Not one isolated squeeze.

A broader truth is surfacing:

more and more parts of the global financial system are behaving as if they are drawing from the same finite pool of liquidity, collateral, and real metal.

That is why this feels so unstable.

Japan is straining.

Private credit is gating.

Silver float is tightening.

Hormuz is evolving from a headline into a structural choke point.

China is buying weakness.

India is deepening the monetary role of metals.

These are not separate stories.

They are connected pressure points inside the same overstretched system.

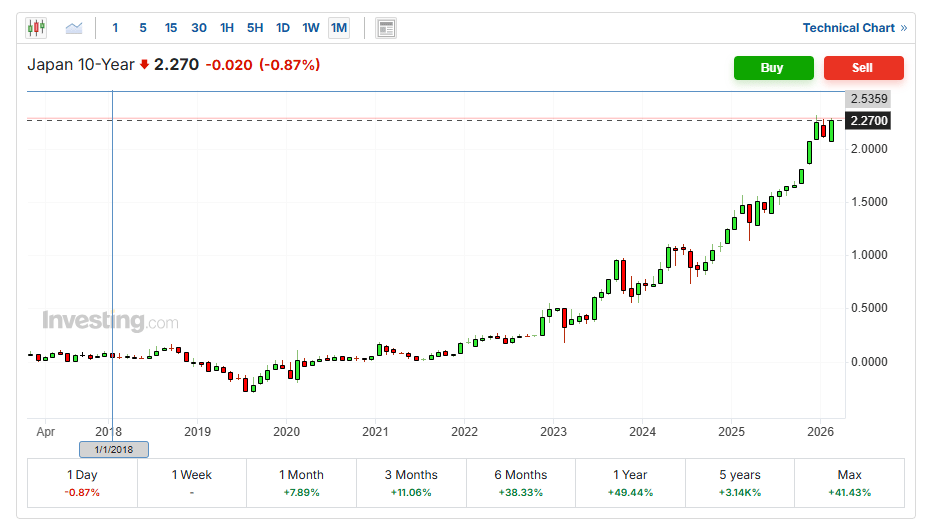

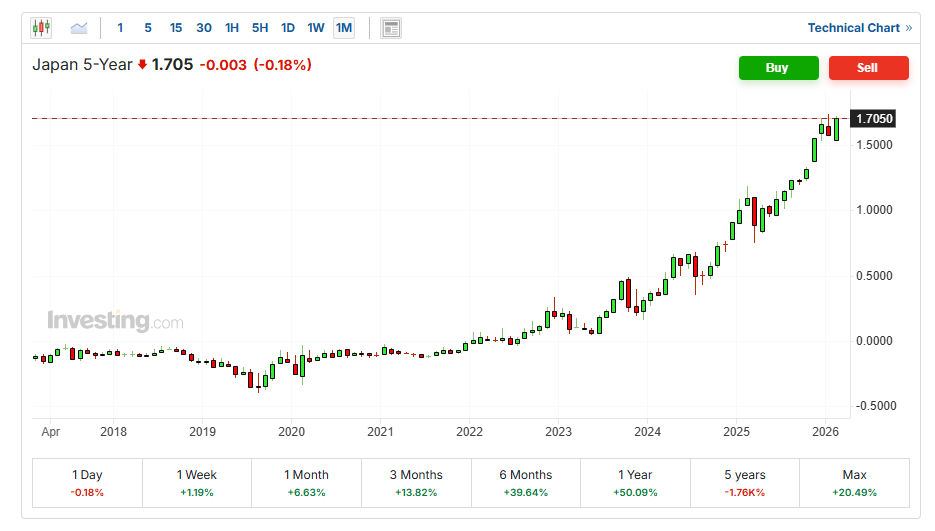

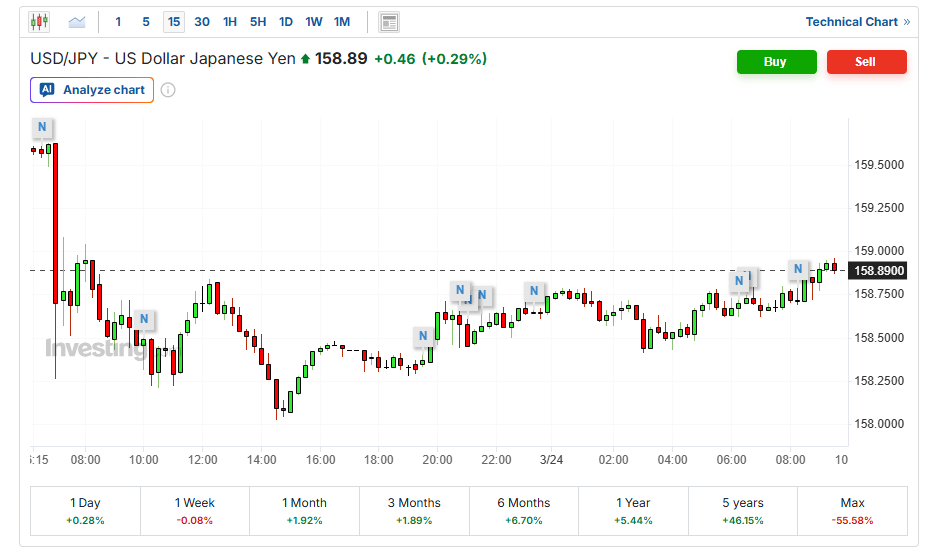

Japan is not a side story. It is a core funding story.

The move in Japan is not background noise.

Japan 10Y is now around 2.27%–2.30%.

Japan 5Y is near cycle highs.

USD/JPY is near 159–160.

And the trigger is obvious: oil/Hormuz stress feeding imported inflation into one of the world’s most important cheap-funding economies.

That combination is toxic.

When JGB yields rise while the yen stays weak, Japan gets squeezed from both directions:

higher domestic yields,

higher imported energy costs,

and more unstable carry/funding conditions.

That is not just a local Japanese problem.

That is one of the load-bearing walls of global leverage getting stressed.

For years, global markets benefited from a world where Japanese money was cheap, abundant, and structurally suppressive to volatility.

That world is no longer stable enough to be taken for granted.

And when one of the hidden funding anchors of the global system starts wobbling, the effects do not stay in Tokyo.

They bleed outward into bonds, currencies, commodities, risk assets, and credit — all at once.

The physical silver story keeps getting stronger, not weaker.

One of the biggest mistakes people are still making is assuming weak paper price means loose physical conditions.

It doesn’t.

In fact, the new silver screenshots point the other way.

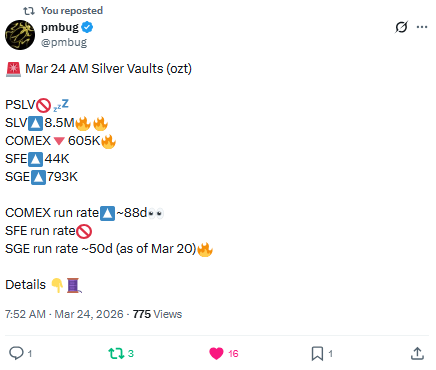

The details matter:

Mar26 contract cumulative deliveries: 8,834

Equivalent ounces: 44,170,000

Actual withdrawals in March: 27,340,758.19

withdrawals currently about 62% of Mar26 delivery requests

That is not trivial.

It suggests real movement matters more than the paper quote implies.

Then you layer in:

SLV share lending activity returning

borrow fee getting more volatile

SLV adding massively

BlackRock and JPM additions

COMEX down 605k oz

SFE up 44k oz

SGE up 793k oz

SFE remaining stock around 11.76M oz

SGE remaining stock around 9.66M oz

run-rate math still implying meaningful draw pressure

That all points to one thing:

this is an interconnected silver system, not isolated pools.

COMEX, SLV, LBMA, SFE, and SGE may look separate on paper.

Under stress, they behave more like connected reservoirs with metal moving where pressure is highest.

That is exactly why lease rates matter so much.

Not because they prove imminent failure.

Because they show the system is increasingly being balanced through mobilization, not abundance.

And that distinction is everything.

A market that is comfortable does not need to keep mobilizing float.

A market that keeps mobilizing float is telling you the cushion is thinner than it looks.

China and India are making the physical side even tighter.

This is where the bullish case becomes much more powerful.

China just pulled 790+ tonnes of silver in 2 months, an 8-year high.

Chinese buyers also lined up for gold on the price decline.

India is beginning to use silver as collateral in lending on April 1.

That combination is huge.

China buying weakness in gold while silver demand stays strong means physical appetite is not fading.

India adding collateral utility to silver means silver is becoming more deeply monetized.

That is not just commodity demand.

That is monetary and financial deepening of demand.

And that matters because once a metal becomes not only industrially useful but also increasingly usable as collateral, the available float can tighten much faster than people expect.

This is exactly the kind of development the paper market tends to underestimate until it can no longer do so.

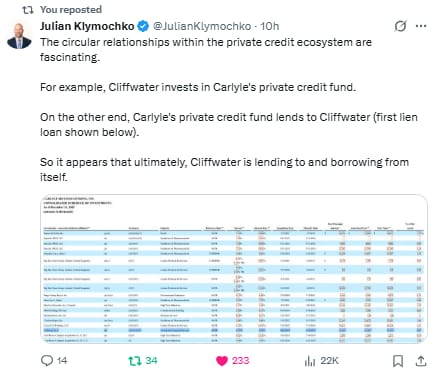

Private Credit Is Not Just Illiquid. It Is Increasingly Circular.

This is not just about funds limiting withdrawals.

It is about a structure that is becoming visibly circular.

If Cliffwater invests in Carlyle’s private-credit fund, while Carlyle’s private-credit fund lends back to Cliffwater, then the system is not just originating credit.

It is increasingly recycling risk inside itself.

That is a much bigger warning.

Because when capital is circulating through interconnected funds and vehicles, the marks can look stable right up until someone asks for real liquidity.

Then the whole illusion gets stress-tested at once.

That is why private-credit gating matters so much.

It is not merely a redemption story.

It is the market discovering that some portion of “yield” may have been supported by circular relationships, internal financing loops, and the assumption that money would keep moving around the same ecosystem.

That is the same broad lesson we are seeing in metals.

Private credit is showing the gap between book value and real liquidity.

Silver is showing the gap between paper exposure and real metal.

Different markets.

Same regime.

Too many claims. Too much internal recycling. Not enough instantly accessible reality.

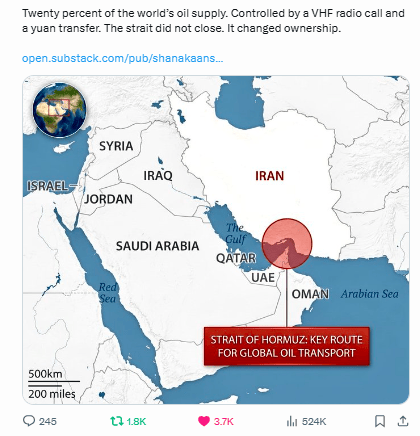

Hormuz is evolving from geopolitical headline to structural system stress.

The Strait of Hormuz story is becoming bigger than “oil might spike.”

If ships are effectively paying for passage, if settlement starts tilting toward yuan, if fuel rationing is spreading, and if supply chains and fertilizer/ammonia flows are getting hit, then this is not just an “oil up / oil down” story.

It becomes:

energy chokepoint stress,

currency implications,

trade-settlement implications,

and inflation/funding consequences all at once.

That matters because the oil shock is not the disease.

It is the accelerant moving through a debt-heavy, globally levered structure.

And that is what makes this so dangerous.

This system was built on three assumptions:

cheap energy,

low rates,

and abundant liquidity.

Now all three are under pressure at once.

That is why what looks like a geopolitical event on the surface is increasingly a macro-liquidity event underneath.

The complacency/risk setup still looks dangerous.

Access the Signal Behind the Distortion

Debt-fueled distortions are warping stocks, credit, and global liquidity. We track the structural signals building beneath the surface — gold, silver, and the asymmetric setups mainstream coverage overlooks.

Already a paying subscriber? Sign In.

Reply