- The Sovereign Signal

- Posts

- Judy Shelton Proposes A Gold Convertible Bond to US Treasury Secretary as US Treasury Market Dysfunction Ramps Up, Global Equities Sell Signal Triggered For 7th Straight Month, Japan Banking Crisis Pushes Global Margin Call Closer, A Billionaire Just Bought 1.5% of Annual Silver Supply

Judy Shelton Proposes A Gold Convertible Bond to US Treasury Secretary as US Treasury Market Dysfunction Ramps Up, Global Equities Sell Signal Triggered For 7th Straight Month, Japan Banking Crisis Pushes Global Margin Call Closer, A Billionaire Just Bought 1.5% of Annual Silver Supply

Luke Lovett

February 16, 2026

Sound Money Shelton has the ear of Treasury Secretary

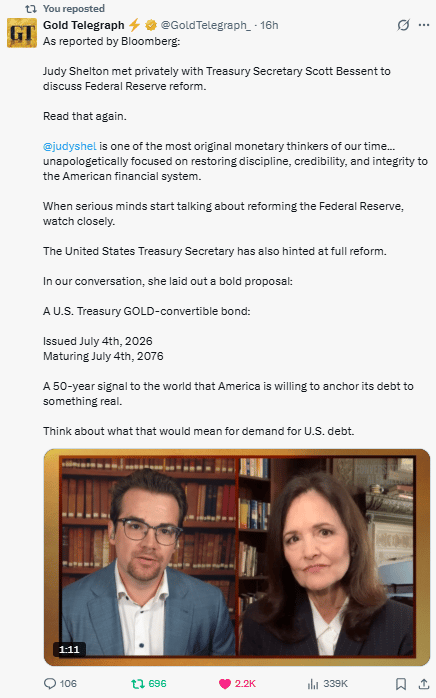

Bloomberg reports that Judy Shelton had an hourlong meeting with **Scott Bessent spanning “Fed reform and international monetary issues,” per Shelton; Treasury didn’t comment.

That alone matters because Shelton isn’t “rate-path commentary.”

She’s “rewrite the constitution of money” commentary.

If the U.S. seriously explores a gold-convertible Treasury instrument, it’s implicitly admitting:

Treasuries alone are no longer sufficient as the unquestioned base-layer trust asset at today’s issuance scale, and

the only way to harden that base layer is to graft on an external settlement anchor.

That graft forces gold to be repriced upward because the conversion price must be high enough to be credible — otherwise the policy collapses under its own arbitrage.

Key Takeaway: gold revalues higher as a function of system design, not just speculation… while the collateral regime attempts to re-ground itself in something markets treat as “hard.”

🚨 This is not normal.

Primary dealers are now sitting on a RECORD $482B of Treasuries.

Why?

Because the Fed is doing QT.

Because debt issuance is exploding.

Because real buyers aren’t stepping up fast enough.

So the dealers are forced to absorb the overflow.

That’s not “healthy demand.”

That’s a system straining under its own weight.

When the institutions required to backstop the Treasury market are maxing out inventory, it tells you one thing:

⚠️ Liquidity is thinning.

⚠️ Funding stress is building.

⚠️ The bond market is getting fragile.

And if the Fed eventually has to step back in?

That’s not stability.

That’s monetization.

This is what late-cycle debt stress looks like before it becomes obvious to everyone.

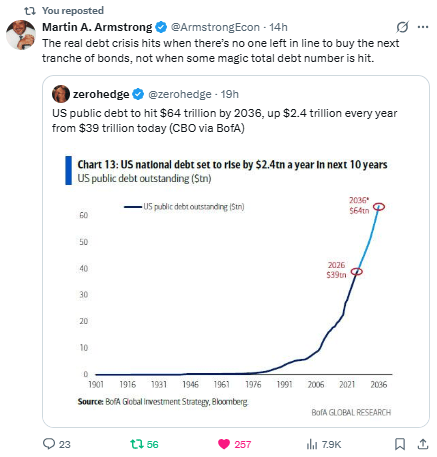

This is the trapdoor under the whole system: the sovereign debt crisis doesn’t “hit” when the debt number gets big — it hits when there’s no marginal buyer for the next auction.

And the Congressional Budget Office baseline is basically screaming that supply pressure is compounding: U.S. public debt is projected to climb toward ~$56T by 2036 (~120% of GDP), with deficits staying structurally large.

If demand balks, the system’s “practical” answer is almost never “let yields clear brutally.”

It’s some form of monetary accommodation—explicit QE, stealth liquidity, or regulatory/structural buyer creation—because letting the Treasury market seize is letting the global collateral backbone crack.

That’s exactly how you exacerbate the global sovereign debt problem: once the world sees the reserve issuer leaning harder on monetization/financial repression, every other sovereign’s cost of capital and credibility gets stress-tested in sympathy.

Gold and silver love that movie.

Not because “the Fed buys it all” is guaranteed—but because the probability-weighted path becomes: more issuance → more dysfunction risk → more intervention → lower real purchasing power of fiat over time.

Gold reprices first as the credibility hedge; silver follows with higher volatility as the “beta” monetary metal.

The chart from Global Markets Investor is basically a positioning + dry powder indicator:

When institutional cash is very low, investors are maximally deployed.

That means:

Less marginal buying power left to push prices higher.

More fragility: when something breaks, there’s less cash cushion—so risk has to be reduced by selling, not by “just holding cash.”

Bad asymmetry: upside becomes grindy, downside exponentially grows for the market to find equilibrium.

So the “sell signal” isn’t prophecy.

It’s a statement about forward return distribution:

Lower expected returns

Higher probability of fat-tail drawdowns

Higher sensitivity to shocks (because positioning is tight)

Also note the phrasing: “triggered for the 7th month straight.”

That’s a classic hallmark of late-cycle melt-up dynamics: the market can remain fully invested for a long time… until a catalyst forces a rebalance.

This “sell signal” is basically the market admitting:

“We’re fully invested, fully confident, and one shock away from needing liquidity.”

That’s exactly the kind of setup where a correction doesn’t just reprice stocks—it pressures policymakers into response mode.

And the moment the story becomes “response,” gold starts looking that much better as the base-layer asset again… while silver becomes the wild overclocked version of the same thesis.

The key is: a more extreme correction tends to produce a more extreme policy response—and that is bullish for the monetary complex over the medium horizon.

Japan doesn’t have to implode to detonate global risk assets.

If the JGB/yen regime shifts hard enough to force a carry unwind, it becomes a global margin call machine — tightening dollar liquidity, pressuring Treasuries, and dragging risk assets into forced deleveraging.

The system is increasingly positioned for a global margin-call style deleveraging event—where funding tightens, correlations collapse, and liquidation becomes mandatory.

In that sequence, policymakers are incentivized to respond with larger-than-ever liquidity measures to preserve market functioning.

That “convex” response function is precisely why gold (and, with higher volatility and lag, silver) should reprice meaningfully higher over time in fiat terms: each rescue stabilizes the present while quietly cheapening the unit of measurement.

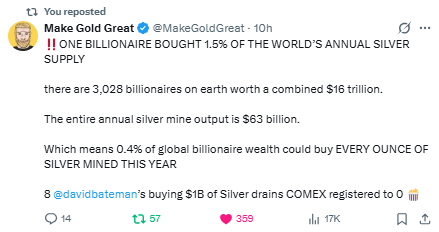

Silver doesn’t have to “run out” to go vertical — it just has to keep doing what it’s been doing:

living in a structural deficit while incremental capital shows up at the margin.

We’re now staring at a projected 6th consecutive year of a supply deficit in silver.

If even a small slice of billionaire wealth tries to move into physical silver, the price doesn’t edge up… it teleports upward until sellers appear.

It only needs a regime shift where large pools of capital—especially ultra-wealthy allocators—begin treating physical silver as a monetary diversification asset.

The investable float is small relative to potential incremental demand, so the market can’t absorb new bids smoothly.

That’s the real “free float” choke point: when a market is already being balanced by inventory leakage, it doesn’t take “all billionaires” or “all supply” to break the clearing mechanism — it takes a relatively small, persistent wave of new physical demand to force a repricing until sellers emerge (or demand is rationed by price).

Why I Use HardAssets Alliance

HardAssets Alliance provides:

100% insurance of metals for market value

Institutional-grade daily audits and security

Best pricing — live bids from global wholesalers

Fully allocated metal — in your name, your bars

Delivery anytime or vault-secured across 5 global hubs

Luke Lovett

Cell: 704.497.7324

Undervalued Assets | Sovereign Signal

Email: [email protected]

Disclaimer:

This content is for educational purposes only—not financial, legal, tax, or investment advice. I’m not a licensed advisor, and nothing herein should be relied upon to make investment decisions. Markets change fast. While accuracy is the goal, no guarantees are made. Past performance ≠ future results. Some insights paraphrase third-party experts for commentary—without endorsement or affiliation. Always do your own research and consult a licensed professional before investing. I do not sell metals, process transactions, or hold funds. All orders go directly through licensed dealers.

Reply