- The Sovereign Signal

- Posts

- Record SOFR Spread Volume, Swap Lines Being Pre-Wired, and $25B Month-End Equity Selling: The Plumbing Is Easing While the Narrative Still Says Tight

Record SOFR Spread Volume, Swap Lines Being Pre-Wired, and $25B Month-End Equity Selling: The Plumbing Is Easing While the Narrative Still Says Tight

The market is telling us policy is restrictive—but the plumbing is quietly doing the opposite. Record SOFR spread positioning, emergency dollar swap lines being lined up behind the curtain, and a mechanical $25B equity seller arriving on schedule all point to the same reality: liquidity stress is already forcing the system to adapt. By the time the narrative catches up, the repricing will already be underway.

Luke Lovett

April 24, 2026

Two days ago we laid out the Two Clocks, One Blockade thesis — Kharg's reservoirs tipping into permanent damage by April 26, Europe's jet fuel running out by May 28, both clocks timed to end inside the window Trump's indefinite ceasefire extension protects.

Yesterday we followed the Medallia tombstone into the mark-to-myth regime — 51 of 52 sovereigns above 130% debt-to-GDP have defaulted, the dollar at 45% of reserves, and the PE industry petitioning the SEC to dump private credit bags into 401ks before the maturity wall hits.

Today the feed is doing something subtle but important.

The clocks haven't stopped. The plumbing has started answering them.

And the answer is coming through silver — the one market that mirrors, in physical ounces, every lie being told in paper.

1. Silver Is The Mirror — And The Mirror Is Shaking

Six years of structural deficit.

Inelastic supply (70% byproduct — you can't just drill more silver, you have to drill more copper, lead, and zinc to get it).

Industrial demand that goes up every time Europe tries to electrify or an AI datacenter gets plugged in.

And now — finally, after a decade of dormancy — a monetary bid returning on top.

That is the constraint no one on CNBC can see. And this week it started speaking.

First, the capitulation: a week-long 30% correction in silver after a month-long parabolic rally.

Hajiyev nailed the psychology at 2 AM — "most of the investors do not have a stomach" for what just happened.

Retail dumped the insurance policy into a managed flush.

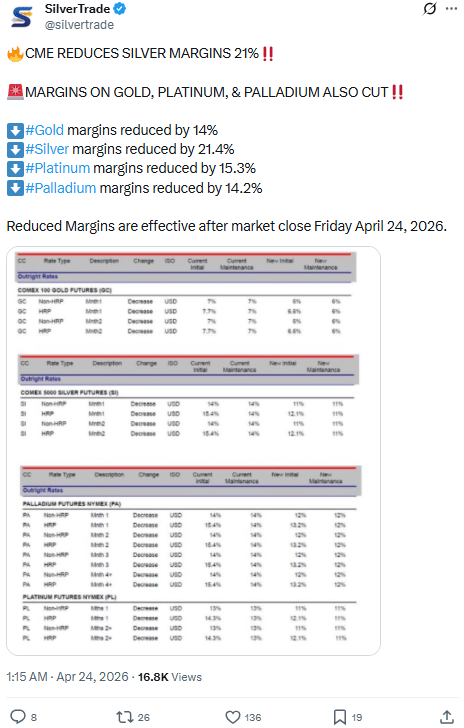

Then the mechanical tell: CME cut silver margins 21.4%, gold 14%, platinum 15.3%, palladium 14.2%.

Exchanges do not cut margins at tops. They cut margins when the forced deleveraging is done and they want liquidity back.

Rafi Farber called it for what it is — "another bottoming signal."

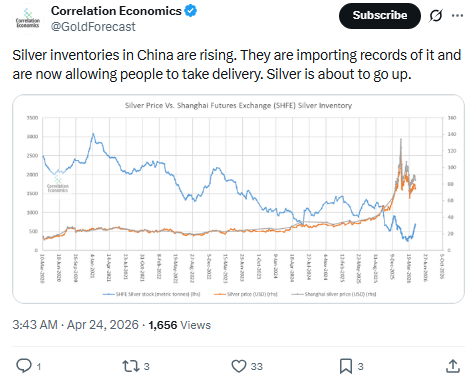

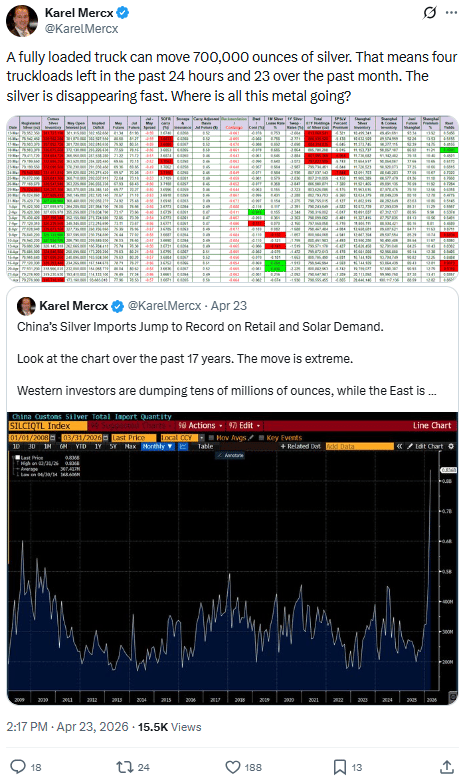

Then the physical: China imported records of silver.

SHFE inventories up 14 sessions in a row to 644 tons.

Beijing is now allowing delivery.

700,000 oz per truck — four truckloads out the Western door in 24 hours, 23 in the past month.

Tie this back to the Shanghai premium we’ve been tracking ($11 over London, EFPs inverted, Deutsche Bank's house account stopping 442 of 480 April silver notices): Western paper is feeding Eastern physical, and they're cutting margins to make it easier to do it again.

The mirror is showing us the answer.

The system needs silver to be dead right now because a live silver re-prices every piece of collateral above it.

2. The Leverage Layer — Yesterday's Thesis, Today's Confirmation

We said Medallia was the first chunk of the corporate interest wall. Today's tape confirms:

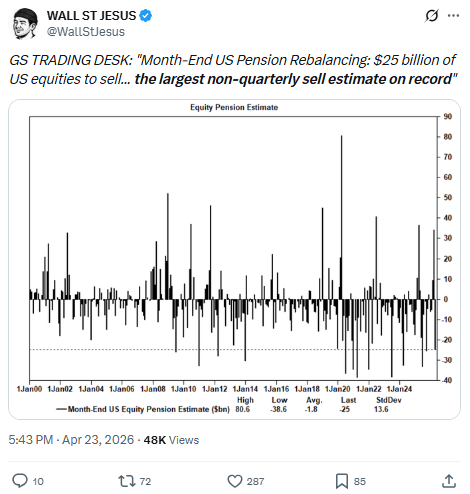

Goldman's pension-rebalance desk: $25B of US equities to sell into month-end — the largest non-quarterly sell estimate on record.

That's not a forecast.

That's a mechanical, calendar-driven, forced seller showing up in six trading days.

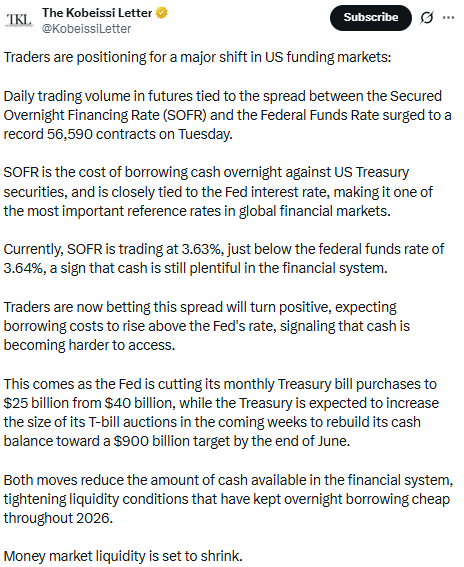

SOFR-Fed Funds spread futures: record 56,590 contracts Tuesday.

The market isn't trading rates anymore — it's hedging the plumbing.

European sovereign spreads widening (Great Martis yesterday) — same picture today, coiling.

Andurand's hedge fund -52% in two weeks on levered oil.

The first body floats.

JPMorgan: "Something is off with the global oil math."

Translation — paper oil is not equal to real oil.

Same story we told about COMEX May oil open interest collapsing 67% in a session.

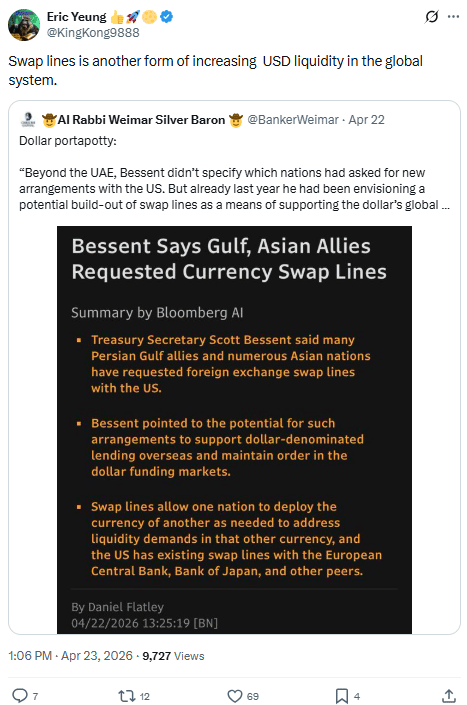

And underneath it all — Eric Yeung spotted it at 2 PM: "Swap lines is another form of increasing USD liquidity in the global system."

Bessent already confirmed Gulf and Asian allies have asked for swap lines.

That is the Fed's invisible QE rail being pre-wired, quietly, while the SP prints new highs on six AI names.

This is what the endgame of a debt super-cycle looks like in public.

Overt tightening on the screen, covert easing through the plumbing. And silver knows.

3. The Real Economy Is Already In The Recession

US Real PCE slowest growth since 2020 — matches the 2001 recession print.

Transports -13% from highs — classic canary, already flying.

Credit card 90-day delinquencies through the 2009 high.

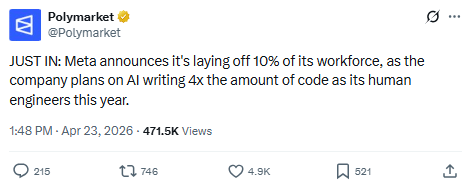

Meta laying off 10% — "AI will write 4x the code" — so the AI capex boom is simultaneously the thing holding up the multiple AND the thing gutting the labor market funding the multiple.

Hedgeye: Less than 1/3 of US workers say now is a good time to find a quality job, down from 70% in 2022.

UK consumer sentiment: gloomiest since records began in 1978.

Buffett: waiting. March was "nothing."

4. The Energy & Food Layer — The Blockade Is Still The Story

The two clocks are still running:

Iran has deployed additional mines in the Strait of Hormuz (Axios via Spectator Index, 13h).

Israel's Katz: "poised to resume the war."

Trump rules out nuclear strike — which is not de-escalation, it is the blockade continuing as the preferred weapon.

Lebanon-Israel ceasefire extended 3 weeks — buying the blockade more runway, exactly as our "indefinite extension is an invoice" framing predicted.

Meanwhile the commodity mirror keeps cracking:

Urea doubled to $900/ton — highest since 2022.

Saudi Arab Light at a record +$28 over Brent.

Sulfur and ammonia shortages now mentioned on the feed (tleilax: "Forget about oil and natural gas prices.").

Michael Hudson: "The #1 US export for 5 months straight is gold… the empire is liquidating itself."

That last one lands with force.

The country that used to export dollars and Treasuries now exports gold. The reserve-currency signal is running in reverse.

And silver — the poor man's gold, the industrial metal, the monetary metal — sits one repricing behind it.

5. The Synthesis — Why Silver Is The Nexus Of The Great Re-Pricing

Access the Signal Behind the Distortion

Debt-fueled distortions are warping stocks, credit, and global liquidity. We track the structural signals building beneath the surface — gold, silver, and the asymmetric setups mainstream coverage overlooks.

Already a paying subscriber? Sign In.

Reply