- The Sovereign Signal

- Posts

- The Floor Is Moving: Treasury Volatility, Private Credit Stress, and Collateral Instability Are Converging

The Floor Is Moving: Treasury Volatility, Private Credit Stress, and Collateral Instability Are Converging

Many people expected a simple script: war escalates, oil rises, gold and silver explode higher, equities crack. But that is not how a leveraged system behaves in the early phase of stress.

Luke Lovett

April 06, 2026

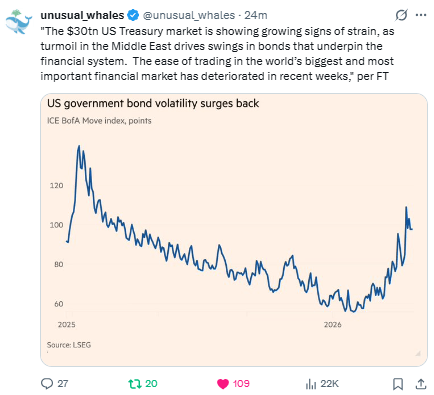

The floor is starting to move

Most people still think of Treasuries as the safe asset.

That is too shallow.

Treasuries are not just “safe.”

They are the base-layer collateral of modern finance.

They set the reference point for global discount rates.

They sit underneath mortgage rates, corporate credit, sovereign spreads, valuation models, repo funding, bank balance sheets, hedge fund leverage, derivatives books, and reserve management.

They are the thing the entire financial superstructure leans on when it wants to call itself liquid, orderly, and well-capitalized.

So when Treasury volatility starts to surge again, this is not some niche bond-market curiosity.

It means the floor itself is moving.

That is what makes the recent move in bond volatility so important. It is not simply telling you that traders are nervous.

It is telling us that the market is becoming less certain about the future path of money, the stability of duration, and the reliability of the very collateral the rest of the system is built on.

That should concern people far more than it does.

Because the structure sitting on top of that foundation is not small, simple, or lightly levered.

It is the largest debt structure ever created.

And it is trying to function while the asset class underneath it becomes harder to trust, harder to intermediate, and more unstable.

If the discount rate itself becomes unstable, everything built on top of it has to be repriced.

And in a levered system, that repricing is unlikely to be mild.

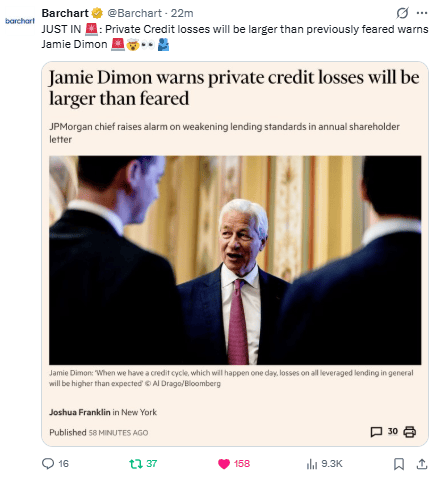

Jamie Dimon is not “connected.” He is positioned at the nerve center.

When Jamie Dimon warns that private credit losses will be larger than feared, the important thing is not celebrity. It is vantage point.

He is not just “well connected.”

He sits close to the center of the machinery that transmits stress before price reflects it.

Global funding flows. Corporate credit pipelines. Private credit distribution. Derivatives exposure. Collateral chains. Liquidity conditions across institutions.

That means he sees things earlier than most of the market sees them.

He sees who is borrowing aggressively. He sees who is struggling to refinance.

He sees where standards are quietly deteriorating. He sees where liquidity is real and where it is merely assumed. He sees where collateral is being stretched.

That is why the warning matters.

Private credit is one of the great concealment mechanisms of the easy-money era. It is opaque. Illiquid. Priced slowly. Marked optimistically. Heavily dependent on stable funding and low volatility.

In other words, it looks stable until it doesn’t.

So when Dimon says losses will be worse than feared, that is not a random comment. It is a signal about the hidden layer of leverage.

And once you place that signal next to rising Treasury volatility, long-end yields refusing to behave, carry stress, commodity tightening, metals being liquidated for cash, and hedge funds reducing exposure, the picture gets much clearer.

The surface changes.

The underlying pressure does not.

First the base layer becomes unstable.

Then funding becomes less predictable.

Then leverage becomes more dangerous.

Then private credit starts to crack.

Then losses appear late, because they were smoothed.

Then liquidity gets pulled.

Then forced selling spreads.

Then policymakers get cornered.

That is the sequence.

And that is why Dimon’s May 2025 warning about a crack in the bond market mattered so much. He was not predicting a headline. He was pointing to the system losing stability at its foundation.

Everything built on top of that foundation eventually feels it.

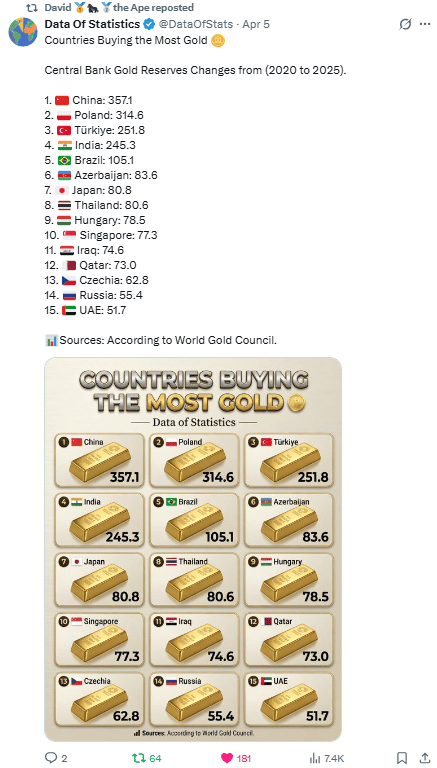

The East is not talking about gold. It is accumulating collateral.

Another chart in the report should make people deeply uncomfortable.

The East is steadily buying gold and securing resources while the West is still intoxicated by paper, narratives, and abstractions. Gold. Resources. Strategic inputs.

That is not just a portfolio preference.

That is preparation.

One side is behaving as if the future will reward ownership of what is real.

The other is still behaving as if leverage, financial engineering, and reserve-currency privilege can indefinitely outrun physical reality.

That gap in behavior matters.

A lot.

Because while the West keeps debating stories, the East keeps accumulating collateral.

And collateral is what matters when trust in the broader structure starts thinning.

Ray Dalio is describing the next phase of monetary fragility

This is also why Ray Dalio’s CBDC comments matter.

Not because it is dramatic. Because it is precise.

He is not simply saying digital money equals control. He is pointing to something more important: money itself is becoming programmable, trackable, and conditional.

That means the question is no longer just what money is worth.

It becomes:

How can money be used?

Who is allowed to use it?

Under what conditions?

Toward what ends?

That is a structural change in the nature of money.

And it is emerging at a very specific moment in the cycle.

Record sovereign debt. Rising interest costs. Less stable bond markets. Inflation that cannot be fully controlled. Political pressure to preserve order. Traditional tools weakening.

Rate cuts are less effective when the long end resists them.

QE carries more inflation risk.

Austerity is politically radioactive.

So the system needs more precise control mechanisms.

That is where programmable money becomes attractive to those trying to preserve stability.

Not because the system is strong. Because it is fragile.

CBDCs allow targeted stimulus. Control over velocity. Flow gating in stress. More direct steering of liquidity. Better maintenance of a debt system that increasingly requires management rather than trust.

From their perspective, it solves real problems.

From a market perspective, it tells you something larger:

confidence in purely financial claims is becoming more conditional over time.

And that has consequences.

It gradually changes what capital begins to value.

Less: what yields the most.

More: what sits outside the system, what cannot be controlled, what cannot be diluted at will, what represents final settlement.

That is why hard assets gain relevance. That is why neutral collateral matters more. That is why gold stops being just a hedge and starts becoming monetary clarity.

The real complacency is in debt markets

Access the Signal Behind the Distortion

Debt-fueled distortions are warping stocks, credit, and global liquidity. We track the structural signals building beneath the surface — gold, silver, and the asymmetric setups mainstream coverage overlooks.

Already a paying subscriber? Sign In.

Reply