- The Sovereign Signal

- Posts

- The Silver Correction Did Not Solve the Silver Problem: Eastern Premiums Stay Elevated as COMEX Registered Collapses 88.2M Ounces From Pre-Blowoff Levels

The Silver Correction Did Not Solve the Silver Problem: Eastern Premiums Stay Elevated as COMEX Registered Collapses 88.2M Ounces From Pre-Blowoff Levels

Most people are still looking at silver through the wrong lens. They think they are looking at a failed blowoff. They think the story is: “Hope you didn’t buy 120.” That is not what this is.

Luke Lovett

March 31, 2026

Most people are still looking at silver through the wrong lens.

They think they are looking at a failed blowoff.

They think the story is: “Hope you didn’t buy 120.”

That is not what this is.

What we are actually looking at is a structural repricing that overshot, corrected violently, and still has not produced the physical relaxation that a true top should have produced.

That is the whole game.

Silver went vertical.

Silver then got smashed.

But after that kind of correction, the physical market should now be behaving like a market that has been cured by lower prices.

It isn’t.

And that is where the analysis gets serious.

The chart already told us something fundamental changed

Start with the monthly, because the monthly is the truth.

Silver did not round-trip back into the old regime. It exploded, corrected, and is still holding at a dramatically higher plateau than the market was conditioned to believe was normal.

That matters.

Because failed manias do not do that. Failed manias collapse back into irrelevance. They reveal that the whole move was mostly air.

This has not.

The monthly structure says something very specific:

silver discovered a much higher clearing zone, overshot it in the first repricing wave, and is now digesting that discovery rather than reversing it.

That is a completely different thing from a dead market.

The technical structure reinforces it. The longer-term trend characteristics are still far too strong to dismiss this as leftover noise from a speculative episode. The signal is not “everything is fine.” The signal is more interesting than that:

the secular move is still alive, but the market is forcing everyone to suffer through the ugly middle.

And the ugly middle is where most people lose the plot.

The real tell is not what happened on the way up

The real tell is what happened after the correction.

If the move from the 120 area down into the low-70s had truly solved the silver problem, then the physical market should now be sending unmistakable signs of normalization.

That is what people mean when they say:

“Price solves everything.”

And in a real market, that is true.

If price goes high enough, physical demand cools.

Inventories stabilize.

Spreads relax.

The shortage begins to heal.

That is how an organic market cures itself.

So that is the real question here:

Did the correction actually solve the problem?

And the answer, so far, is:

NO.

China remains the clearest signal.

If London were telling the truth about where silver clears, Shanghai should not still be trading like this.

But it is.

With LBMA around the low-70s, Shanghai has still been running at roughly a 13% premium to the West.

That is not noise.

That is not some rounding error.

That is not a quirky local dislocation you dismiss with a hand wave.

That is the market saying:

physical silver in Shanghai is still worth materially more than London paper says it is.

That is the message.

And it is an incredibly important one.

Because once a market has already had a huge run and then a brutal correction, the burden of proof changes. The question is no longer whether someone can invent a bullish narrative. The real question is whether the correction actually restored physical ease.

If the correction had done its job, that premium should have compressed much more convincingly.

It didn’t.

Which means the physical market is still not validating the idea that the corrected Western paper price is fully sufficient.

That is not ordinary bullishness.

That is a market still in contested price discovery.

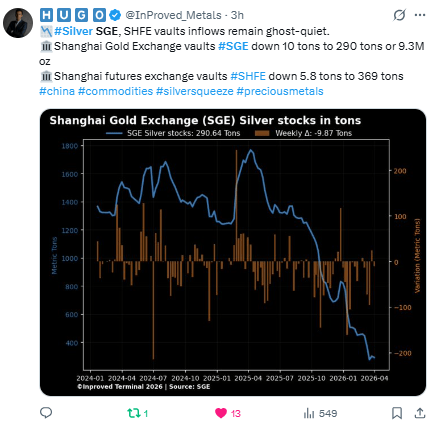

Then look at inventories, because this is where the argument hardens

Premiums matter.

But premiums alone are not enough.

What makes the case powerful is that the premium story is being reinforced by inventory behavior.

Today’s Shanghai data showed:

SGE stocks down another 10 tons to roughly 290.64 tons

SHFE stocks down another 5.8 tons to about 369 tons

Now be precise here.

That does not prove “immediate shortage everywhere.”

It does not mean inventories fall every day forever in a perfect straight line.

But it does tell you something very specific:

even after a huge correction in price, the latest Shanghai data still does not look like a market that has fully relaxed physically.

That matters because, again, price is supposed to solve everything.

If price has gone high enough — and then corrected enough — to cure the problem, physical demand should cool and inventories should begin stabilizing much more convincingly.

Instead, the latest Shanghai data is still showing depletion, not obvious normalization.

That is a serious signal.

The same logic applies to COMEX — and this is where the case gets much harder to ignore

COMEX registered silver was roughly 164.2 million ounces on November 1, 2025, before the move from around $48 into the acceleration phase of the run toward $120.

As of March 30th, registered silver had fallen to 76.02 million ounces.

By March 30, registered had fallen to just 76.02 million ounces.

Read that again.

Silver went from roughly $48 into one of the most dramatic price advances in its history.

Then it suffered a violent correction.

And through that whole sequence, COMEX registered silver still fell by roughly 88.2 million ounces.

That is a draw of about 53.7%.

Access the Signal Behind the Distortion

Debt-fueled distortions are warping stocks, credit, and global liquidity. We track the structural signals building beneath the surface — gold, silver, and the asymmetric setups mainstream coverage overlooks.

Already a paying subscriber? Sign In.

Reply