- The Sovereign Signal

- Posts

- When Interest Costs Top Defense and COMEX Runs Dry: A Data‐Driven Guide to the Coming Currency Sacrifice

When Interest Costs Top Defense and COMEX Runs Dry: A Data‐Driven Guide to the Coming Currency Sacrifice

Interest is now the second‐largest line item in the U.S. budget, quietly overtaking defense while markets party at record valuations. At the same time, COMEX silver stocks have been bled down to historic lows as miners and industrials walk away from the paper game and lock in real metal. This is the story of what happens when the bill for decades of exponentially increasing leverage and under‐investment finally comes due—and why the only thing left to sacrifice is the currency itself.

Luke Lovett

April 16, 2026

The Scene: A Historic Rally Built on a Broken Foundation

The tape looks triumphant.

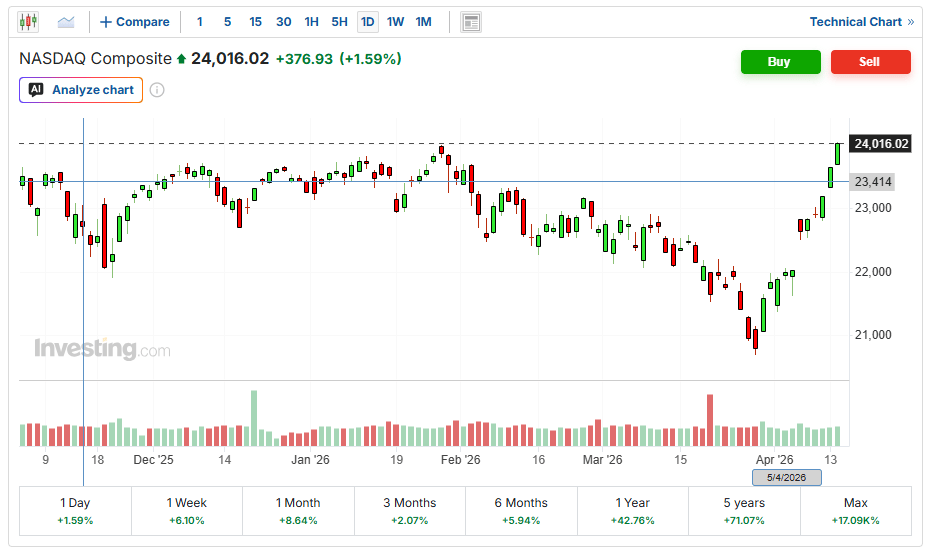

The Nasdaq just logged ten consecutive green sessions — its longest win streak since 2021 — with a roughly +13.7% gain over that stretch, one of the largest 10-day moves since 2009.

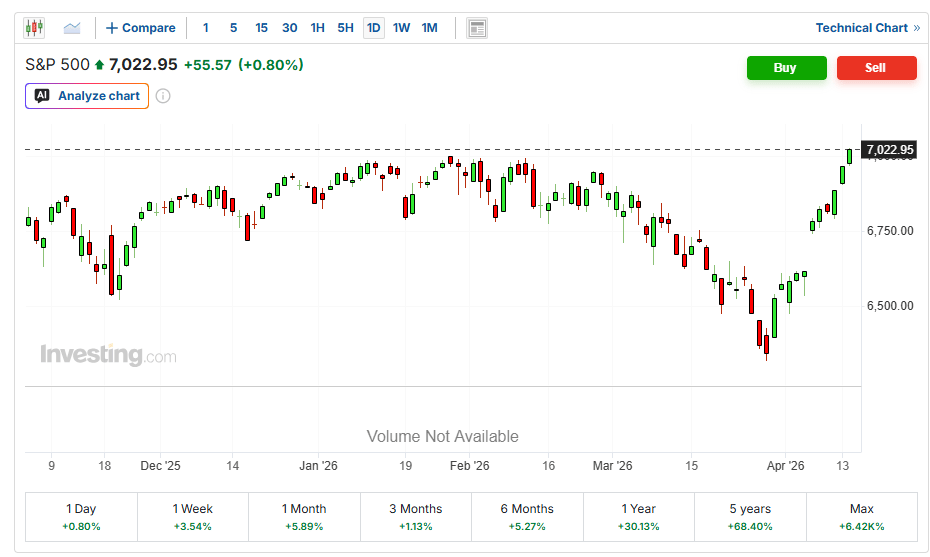

The S&P 500 has been up in nine of the past ten sessions, and headline writers are calling it "one of the best recoveries this century."

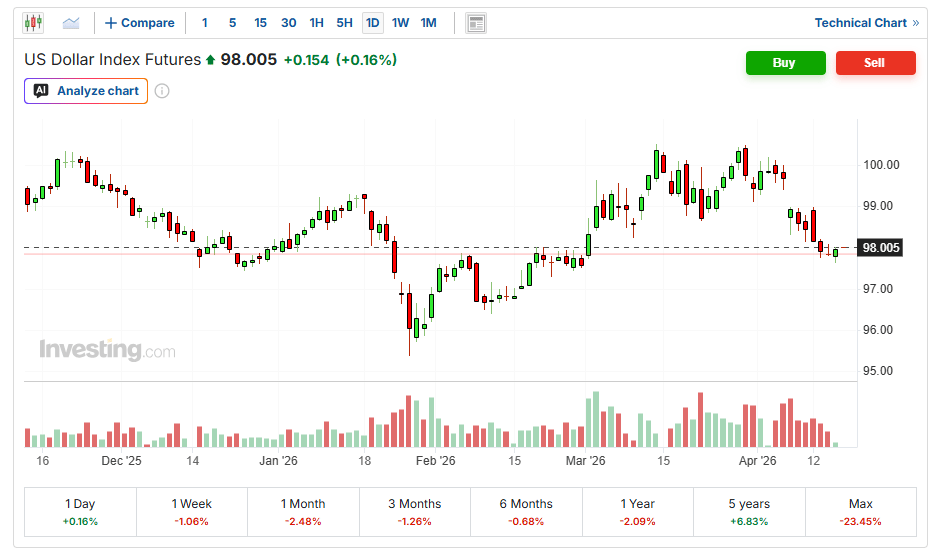

Meanwhile, the dollar is rolling over, with the DXY sliding below 98.2 and EUR/USD pushing above 1.16, providing a soft-dollar tailwind that flatters risk assets in nominal terms.

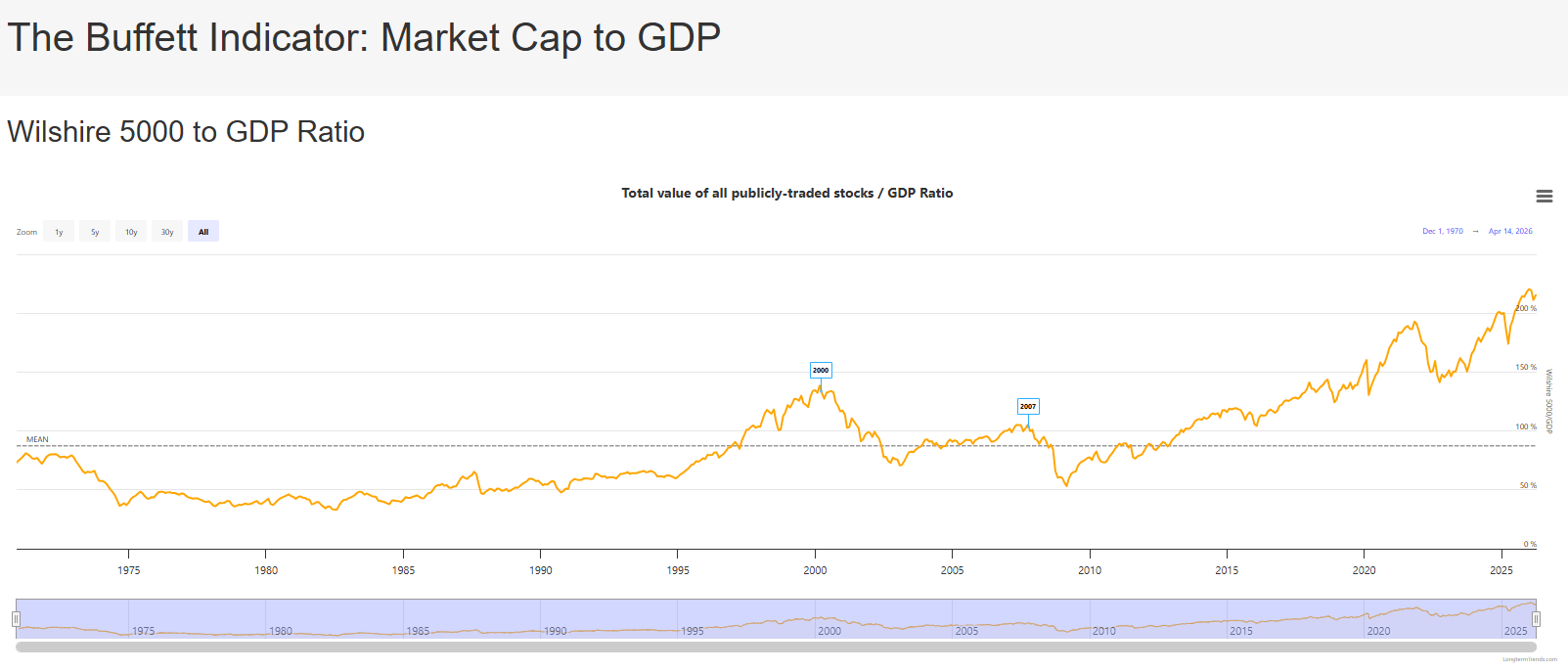

And the Wilshire 5000-to-GDP ratio — Warren Buffett's preferred macro valuation gauge — has just hit 223.55%, a level never seen before in recorded history, eclipsing both the dot-com peak and the 2021 post-pandemic surge.

The rally did not restore fair value.

It drove valuations to the most stretched extreme on record, at exactly the moment the world's most decorated value investor is sitting on nearly $400 billion in cash, mostly T-bills, and now owns more short-duration government paper than the Federal Reserve itself.

That is not the behavior of someone who believes equities are cheap.

That is someone preserving maximum optionality and waiting for something to break.

Section I: The Sovereign Balance Sheet Is Already Broken

The fiscal math beneath the market rally is not a future risk. It is a present condition.

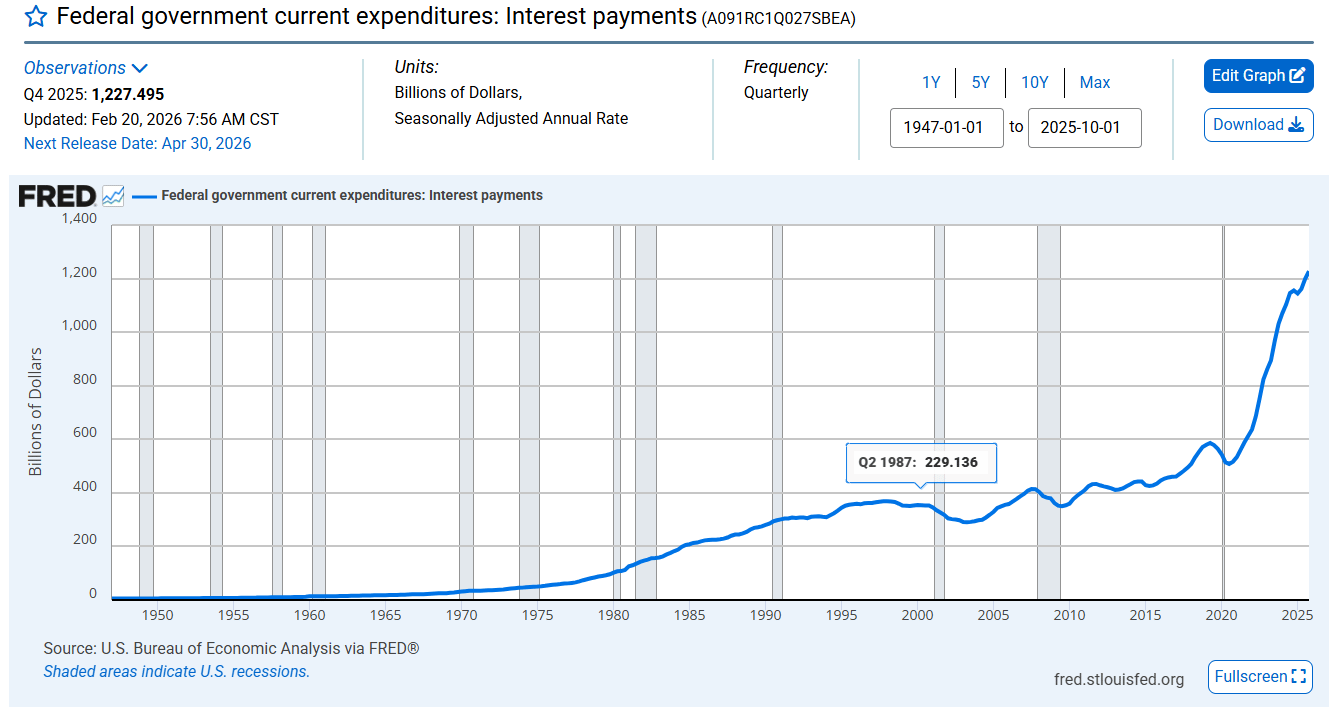

US federal interest expense in the first six months of FY2025 hit $623 billion, up 7% year-over-year and the highest ever recorded for that period.

On a trailing twelve-month basis, gross interest cost runs at roughly $1.3 trillion — now the second-largest line item in the entire federal budget, behind only Social Security at ~$1.6 trillion, and larger than both health programs and defense spending individually.

To put that in context: the US government is spending more on servicing old debt than on the military, more on interest than on Medicaid, and more on the cost of past borrowing than on almost anything it does in the present.

This is the arithmetic of a sovereign that has already spent its future.

The options for resolving it without explicit default are few: grow fast enough to outrun the debt, inflate it away, or use financial repression — holding rates artificially below the inflation rate — to erode the real value of the outstanding claims.

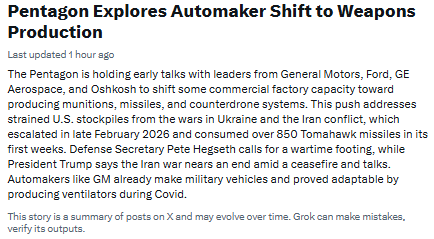

At the same time, the administration is pressing for more spending, not less.

The Pentagon has approached major automakers including GM and Ford about ramping weapons production, a signal that the defense-industrial base is being asked to scale up, not down.

The Treasury has simultaneously been leaning on the World Bank to accelerate critical-minerals projects that diversify supply chains away from China — effectively extending US sovereign credit and influence deeper into the resource sector as a strategic weapon.

The system is being asked to fight a resource and technology cold war while carrying a balance sheet where interest expense is already the second-largest program.

Something must absorb that contradiction. History suggests it is always the currency.

Section II: The Rates Debate — Bessent, the 2008 Analog, and Its Limits

Treasury Secretary Scott Bessent told WSJ's Paul Gigot:

"The Fed has been wrong on inflation and the core inflation is coming down, but I understand if they want to wait until the data's clear, but that will mean that interest rates should come down a lot more."

Mr. VIX (on X), one of the sharper macro voices tracking this dynamic, agrees: the longer rates stay higher, the further they will eventually have to fall.

The historical precedent Bessent's camp points to is 2008: elevated oil prices in the first half of that year ultimately compressed core CPI by destroying demand broadly enough to trigger a deflationary bust, which forced emergency rate cuts.

Oil, in that reading, was the catalyst for disinflation, not sustained inflation.

But that analogy has a flaw that a critic on the same thread identified bluntly: "Elevated oil and a cold war with China is not going to push yields down."

The 2008 demand collapse happened in a world with no active industrial policy to sustain spending, no reshoring mandate, no defense-production ramp, and no explicit resource-security program.

The cold war constraint set creates a structural floor under both inflation and yields that simply did not exist in the purely cyclical 2008 episode.

The resolution of this tension is probably not "clean rate cuts" but something uglier: rates held below the inflation rate for an extended period — financial repression — which erodes the real value of the debt stock while nominally leaving rates positive.

Bessent's own words — "rates should come down a lot more" — are, whether intentionally or not, a forecast of negative real rates ahead.

That is the most direct statement imaginable from a Treasury Secretary that the plan is financial repression.

Holders of long-duration paper, take note.

Section III: Real-World Constraints — Energy, Food, and a Decade of Starved Capex

The macro backdrop that gives financial repression its bite is a physical world that has been under-invested for a decade and is now being stress-tested by war.

Energy: The Middle East shock has removed a significant slice of production from the system, and Washington's behavior — arming allies, mobilizing industrial capacity, patrolling chokepoints — signals this is not a temporary headline event.

A structural geopolitical risk premium is being welded onto the barrel for years, not weeks.

Fertilizer: Urea has ripped back toward prior extremes, approaching the $700+ per ton range after a round-trip from 2022's spike, collapse, and now renewed surge.

Fertilizer is natural gas in another form; when it moves like this, future food costs are being quietly repriced with a multi-year lag.

And as was noted starkly this week: there is no strategic reserve of fertilizer — unlike crude oil, there is no SPR-style buffer for the input that sits between natural gas and global food production.

The US built alphabet-soup liquidity facilities for banks and an oil reserve for energy security, but the input that feeds most of the world has no buffer at all.

Mining capex: Gold and silver miners' capital expenditure, adjusted for prevailing metal prices, remains deeply depressed relative to the prior cycle peak — on the order of 80%+ below former highs.

After a decade of financialized comfort with just-in-time everything, the world finds itself asking a supply side that never reinvested to suddenly meet war-time demand.

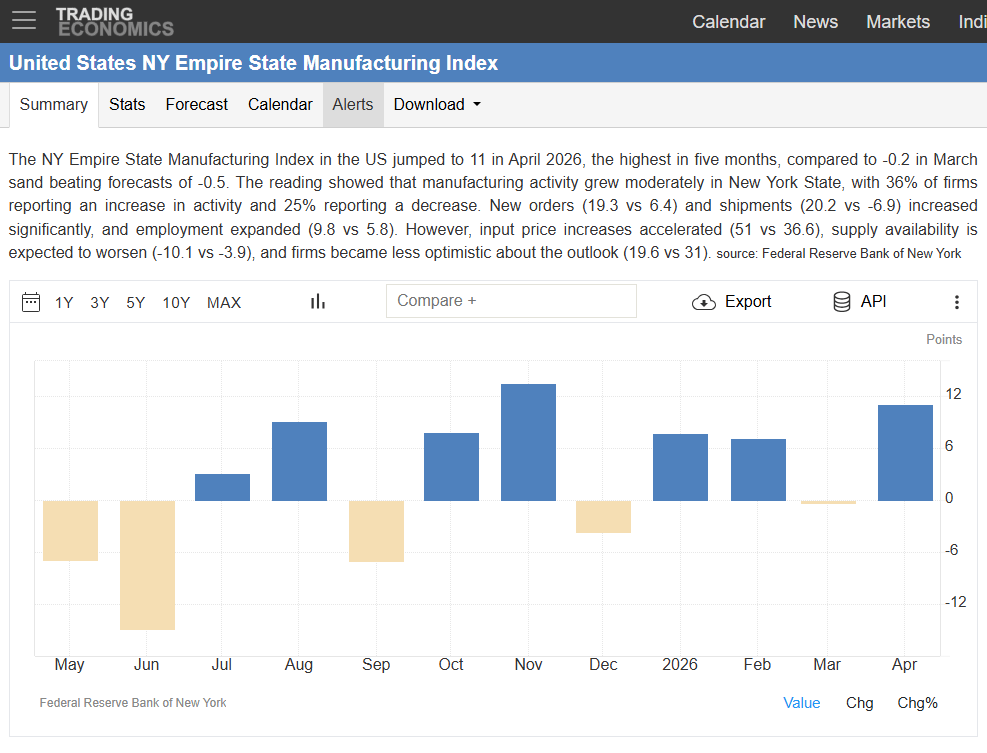

The NY Empire State Manufacturing Index printed +11.0 in April versus an estimate of +0.3 and a prior reading of -0.2, confirming that factory activity is re-accelerating into the war and into high oil prices.

The likely driver is defense, infrastructure, and reshoring orders rather than organic consumer-led demand.

The important implication: war-time policy is propping up industrial demand for metals, energy, and materials at the exact moment that supply is most constrained.

That is not disinflationary. That is the opposite.

Section IV: Silver's Great Exodus — The Paper-Physical Divorce in Real Time

Silver is not merely a commodity trade right now.

It is a live stress test of the entire paper-claims model, playing out in the open with CME warehouse data as the evidence.

The Vault Drain

CME warehouse reports as of April 14, 2026 show registered (deliverable) silver at approximately 76.9 million ounces — down sharply from over 200 million ounces at late-2025 peaks and from roughly 86 million ounces in late February 2026.

That is a drawdown of more than 60% in registered deliverable stock in roughly six months, with inflows into the "received" category far too small to offset the withdrawals.

The data creates an unprecedented picture: physical metal is being diverted upstream, before it ever reaches the COMEX pipeline.

Access the Signal Behind the Distortion

Debt-fueled distortions are warping stocks, credit, and global liquidity. We track the structural signals building beneath the surface — gold, silver, and the asymmetric setups mainstream coverage overlooks.

Already a paying subscriber? Sign In.

Reply