- The Sovereign Signal

- Posts

- When the Treasury Band-Aid Fails: Buybacks Amid War on Treasuries

When the Treasury Band-Aid Fails: Buybacks Amid War on Treasuries

While foreign central banks hold more gold than U.S. debt for the first time since 1996, the U.S. Treasury is buying back billions of its own IOUs to keep the machine from stalling. Together, they reveal the most asymmetric wealth reallocation in modern history — from a 54-year-old experiment in debt to the millennia-old foundation of gold and silver.

Luke Lovett

August 29, 2025

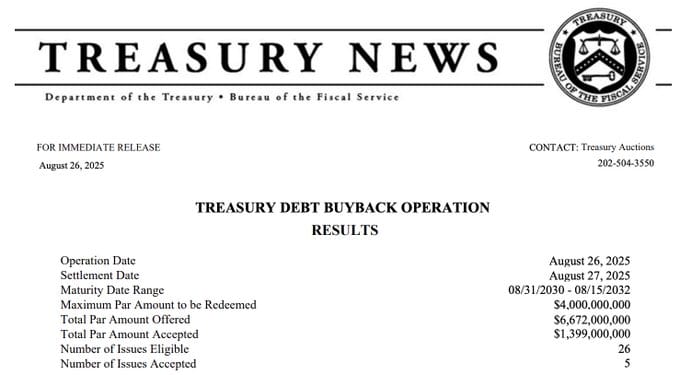

Credit to @Barchart (X) for the above image

The Debt Buyback Announcement (Surface Layer)

The U.S. Treasury just bought back another $1.4B of its own bonds, bringing the total to $7.4B in two weeks.

On the surface, it reads like a proactive strength move: “We’re managing the curve, reducing stress, improving liquidity.”

But zoom out:

What It Really Is

Not debt reduction. These buybacks are funded with new issuance; net debt doesn’t fall.

Collateral upgrade. The Treasury is retiring illiquid, “off-the-run” notes and replacing them with fresh, on-the-run supply that dealers and repo desks actually want to trade.

Translation: It’s about keeping the pipes unclogged, not shrinking the mountain of debt.

Why That Matters

The very need for buybacks is a tell.

If Treasuries (the base layer collateral of the entire financial system) were uniformly liquid, there’d be no need for artificial smoothing.The fact that Treasury feels compelled to intervene is evidence of strain.

Collateral upgrades are not free.

Each time the government artificially improves collateral quality, it allows more leverage to pile on top of that “better” collateral.

→ That increases systemic dependency on a smaller and smaller pool of “pristine” paper.Upgrading collateral increases its velocity through the system.

That’s helpful in calm seas, but it also means more leverage layered on the same “hot” collateral.

In stress, the unwind hits harder.

Where Fragility Creeps In (the pro-cyclical point)

Think of it like this:

Higher collateral velocity.

When off-the-run is swapped into on-the-run, that paper suddenly becomes usable across more chains (repo, swaps, ETFs, etc.).It gets re-pledged more times.

→ This boosts leverage capacity, but also raises sensitivity.

Amplification in shocks.

In calm periods, this feels like stability. But when volatility hits:Dealers pull back.

Haircuts rise.

The same “high-quality” collateral that was pledged multiple times suddenly can’t stretch as far.

→ Because velocity was higher, the unwind is sharper. One bond pulled from the chain removes multiple links at once.

Bigger buybacks = bigger dependency.

As debt grows, the share of illiquid, off-the-run bonds grows too. That means buybacks must scale up just to keep pipes smooth.

→ The more the system leans on artificial collateral upgrades, the more fragile it becomes if Treasury ever slows or stops.

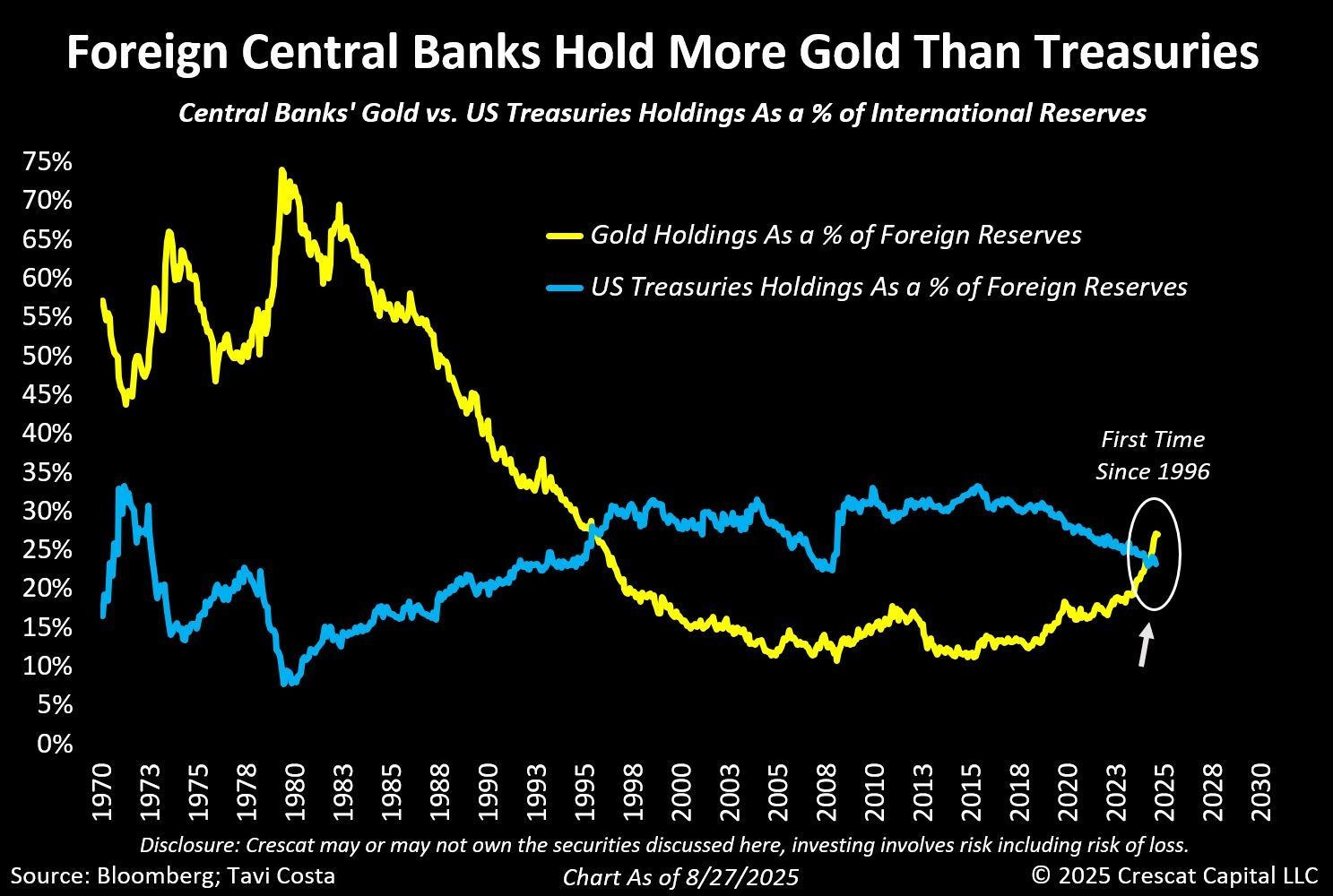

Credit to Tavi Costa/Crescat Capital LLC for the above image

Central Banks Holding More Gold Than Treasuries (The Structural Layer)

Now, layer in the above chart: foreign central banks now hold more gold than Treasuries for the first time since 1996. That’s monumental.

Translation: The world’s most important balance sheets (sovereigns) are reducing reliance on U.S. debt and returning to the true base-layer asset: gold.

Implication: Buybacks look less like strength, more like response to foreign retreat.

If foreigners aren’t rolling Treasuries as reliably, the Treasury itself has to step in and smooth things.

Gold overtaking Treasuries is not just symbolic — it’s a flashing red warning light that the traditional reserve architecture is eroding.

Signal | Latest Level | Interpretation | Zone |

|---|---|---|---|

10-Year Swap Spread | –26.97 bps | Still deeply negative — confirms persistent impairment in cash Treasuries. Dealers continue to prefer synthetic hedges (swaps) over warehousing real bonds. Structural stress signal. | 🔴 Red |

Reverse Repos (RRP) | $31.966B | Hovering near cycle lows — sterilized collateral cushion remains nearly gone. More Treasuries circulating “in the wild,” boosting collateral velocity and fragility. | 🔴 Red |

USD/JPY | 147.06 | Still in the danger band; volatility tripwires at 140/160 remain critical for cross-asset shock potential. | 🟠 Orange |

USD/CHF | 0.8011 | Safe-haven CHF bid remains firm — reflects persistent stress hedging against systemic fragility. | 🟠 Orange |

3-Year SOFR–OIS Spread | 25.8 bps | Elevated and sticky — lenders continue charging a “future anxiety premium.” Signals embedded term funding stress. | 🔴 Red |

SOFR Overnight Rate | 4.36% | Still slightly elevated after ticking up for 3 straight days — confirms funding costs are sticky even as volumes balloon. | 🟡 Yellow |

SOFR Daily Volume | $2.889T | Fresh surge to new highs — system now chained tighter than ever to nightly rollovers. Just-in-time liquidity at redline. | 🟠 Orange |

SLV Borrow Rate | 0.63% (4.1M avail.) | Borrow costs jumped higher with availability slipping — squeeze pressure back on. | 🔴 Red |

COMEX Silver Registered | 197.04M oz | Slight uptick in registered stocks — but cushion remains thin relative to paper leverage. Fragility intact. | 🟠 Orange |

COMEX Silver Volume | 65,458 | Moderate turnover — positioning cooled from peaks but remains active. | 🟡 Yellow |

COMEX Silver Open Interest | 156,112 | Still high, though slightly lighter — leveraged exposure intact. | 🟠 Orange |

COMEX Gold Registered | 21.44M oz | Small uptick — but still wafer-thin versus total paper exposure. Base-layer coverage fragile. | 🟡 Yellow |

COMEX Gold Volume | 173,462 | Strong turnover — positioning rotation robust. | 🟠 Orange |

COMEX Gold Open Interest | 466,024 | Fresh highs in positioning — conviction exposure remains elevated. | 🟠 Orange |

UST–JGB 10Y Spread | 2.608% | Grinding closer to the 2.5% “danger zone.” Below that, carry-trade fragility worsens; above 3%, UST demand weakens. Fragility in both directions. | 🟠 Orange |

Japan 30Y Yield | 3.189% | Near record highs — still exporting stress directly into U.S. Treasuries. | 🔴 Red |

US 30Y Yield | 4.906% | Pressing cycle highs — amplifying debt fragility at the global base layer. | 🟠 Orange |

The Holistic Read: Liquidity Stress + Shrinking Trust

When you put these together:

Treasury Buybacks = Short-term symptom management.

The U.S. is buying its own IOUs back to keep yields from rising.

Central Banks favoring Gold = Long-term regime shift. The foundation of trust in U.S. paper is weakening.

This reveals a paradox:

The Treasury is trying to manufacture liquidity in a system that’s structurally weakening more and more.

That’s like patching potholes on a road while the whole bridge is crumbling underneath.

Why This Matters Right Now

Repo stress already elevated: Overnight funding (SOFR) volumes rolling $2.8T nightly…

This means every Treasury that doesn’t have a natural buyer becomes a funding problem.

Dealer balance sheets thin: Rising long yields mark down inventories and force more balance-sheet rationing.

Buybacks are basically the Treasury saying: “We’ll help you offload the stuff you can’t carry.”

Base layer realignment: Meanwhile, gold demand is climbing, silver deficits persist, and central banks are explicitly moving away from dollar IOUs.

The juxtaposition is striking:

On the surface, buybacks try to soothe nerves.

At the foundation, the world is signaling that U.S. debt is no longer unquestioned reserve money.

Big Picture — What We’re Really Seeing

This isn’t just about smoothing bond auctions.

It’s about a system quietly running out of balance sheet.

Debt buybacks are a bandage.

Gold accumulation is a migration back to bedrock.

One is reactive.

The other is a fundamental shift in the base layer.

The unavoidable conclusion: the pendulum is already swinging.

The more the U.S. props up the Treasury market with band-aids, the more obvious it becomes that gold (and silver) are the real base layers waiting to be repriced.

🔥 Bottom Line

Every debt buyback is evidence of a foundation bending further under exponential strain.

Foreign central banks aren’t waiting for the bend to snap — they’re reallocating to gold now.

The “quiet run” has already begun.

The question isn’t whether the pendulum swings back — it’s how explosively markets reprice when the illusion of debt as a functional base layer finally takes hold.

Not Doom and Gloom — Asymmetry

Every stress signal flashing — $2.8T rolled nightly in repo, a deeply negative 10 year swap spread, Treasury buybacks etc. — isn’t the end of the world.

It’s the sign the old foundation (debt) is cracking. A fundamental shift in motion.

Cracks in debt don’t erase trillions upon trillions in currency — they force reallocations towards the most intrinsically valuable assets.

And for the first time since 1996, central banks now hold more gold than Treasuries.

The smartest money on Earth is already moving back to the true base layer.

Gold and silver don’t need counterparties. They don’t depend on nightly rollovers. They have outlasted every monetary regime.

That’s the asymmetry: a 54-year-old foundation of debt decaying under exponential weight — versus a 5,000-year-old foundation of real value waiting to be repriced.

This isn’t collapse. It’s opportunity — the greatest wealth migration in modern history for those who see it before the herd.

Why I Use HardAssets Alliance

HardAssets Alliance provides:

100% insurance of metals for market value

Institutional-grade daily audits and security

Best pricing — live bids from global wholesalers

Fully allocated metal — in your name, your bars

Delivery anytime or vault-secured across 5 global hubs

Luke Lovett

Cell: 704.497.7324

Undervalued Assets | Sovereign Signal

Email: [email protected]

Disclaimer:

This content is for educational purposes only—not financial, legal, tax, or investment advice. I’m not a licensed advisor, and nothing herein should be relied upon to make investment decisions. Markets change fast. While accuracy is the goal, no guarantees are made. Past performance ≠ future results. Some insights paraphrase third-party experts for commentary—without endorsement or affiliation. Always do your own research and consult a licensed professional before investing. I do not sell metals, process transactions, or hold funds. All orders go directly through licensed dealers.

Reply